To read additional materials about the first modern corporations, please visit this website.

Eighty pragmatic French shareholders in the14th century laid the foundations of modern corporate governance while ensuring their companies’ survival for some 600 years. Their accomplishments resonate today as corporations develop and implement their own approaches to corporate governance and as the reasons behind recent corporate failures are examined.

Embodying entrepreneurial spirit, a group of well-heeled citizens of Toulouse crafted a way to pool their capital, spread their risks and provide a healthy return on their investment. In the process they created a system of corporate governance, risk and compliance focused on mastering the fundamentals. A treatise published some fifty years ago, based on the original medieval records, chronicles how they did it – a process of trial and error coupled with an ingenious system for controlling greedy instincts. What follows are some of the challenges they faced and how they overcame them, along with what abruptly ended their 600 year-old enterprise in the middle of the 20th century.

Risky Business

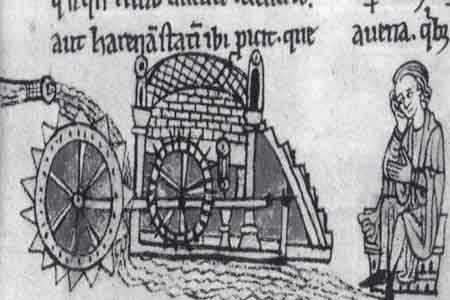

For the operators of water-powered mills in the Middle Ages along the Garonne River, risk was writ large – England’s marauding Black Prince destroying infrastructure and crops, recurring bouts of the Black Death decimating the work force and customer base, iffy harvests and frequent famines making earnings forecasts difficult, a physical plant prone to breakdown and in constant need of costly maintenance, cash flow drying up when droughts slowed the river’s flow, and weak regulation by a central government in far-off Paris – all at a time when a mill was essential to daily life and to the local economy.

Not only did the mills provide power to grind wheat into flour for making bread but also to saw timber into boards for construction and to power machines to do what would otherwise be back-breaking work in a world knowing little innovation since Roman times. Mill companies were essential to the infrastructure and commerce of the region, building dams to increase the speed of the water driving the waterwheel and erecting bridges atop the dams, making it easier to get people and goods to the other side of the river. Uniting self-interest and social responsibility, nascent capitalists banded together to form companies and undertake what no one could accomplish alone, while earning an enviable return on their investment of up to 25% per year.

Managing the Fundamentals

As early venture capitalists, the owners of the mill companies were the movers and shakers of Toulouse society, both landed gentry and wealthy merchants. They were not looking to give up their day-jobs of overseeing vast property holdings, operating banks or weaving cloth, to run a mill. Rather, they were seeking further enrichment by pooling capital and limiting risk while sharing in the profits without day-to-day responsibility for running the business.

In evolving the first governance model, the owners of the mill companies were pre-occupied with the same fundamentals today’s investors would recognize. They appreciated that success depended on wielding their power as owners while confronting and balancing the selfish inclinations of shareholders, employees, suppliers and customers. They attacked this challenge head-on by eliminating what they viewed as one of the biggest risks to their investment – the potential for conflicts of interest born of natural yet greedy impulses. Controls and procedures to keep conflicts at bay, supported by transparency in all aspects of operations and record-keeping, yielded confidence in the companies and steady growth over centuries.

Legal

Beginning in the late 13th century, budding capitalists hit upon joint ownership as a way to pool capital and spread risk, but each investor owned a specific mill asset such as land or the grinding stone. This proved unworkable when owners wanted to dispose of their interests and as costs mounted for maintenance and improvements.

During the 14th century, another attempt was made, this time using the “societas,” a joint ownership arrangement dating back to when the Romans ruled Gaul. Through an audacious leap of faith, it was transformed into a legal person separate from its owners – a company in the modern sense – continuing its existence beyond the lives of shareholders, limiting shareholders’ liability to their paid-in capital, centralizing management in persons empowered to contract on behalf of the entity, and dividing ownership into units of freely transferable shares.

Early on, the shareholders had to confront the fact none of them was inclined to be involved in the messy day-to-day operation of a mill. They needed a way to delegate authority without losing control. Their solution was to elect from among their ranks an eight-member board to hire and supervise a general manager. To prevent the board from gaining the upper hand and eclipsing the interests and ultimate authority of all the shareholders, board members were elected two at a time to two-year terms with term limits.

Having put in place the basic legal framework to make their enterprise work, the shareholders faced a challenge familiar to today’s investors – legal disputes and the attendant role of government. For example, the government intervened when one mill company sought to merge with its only remaining competitor, sensing that a monopoly would lead to a spike in the price of bread and the likelihood of a rebellious peasantry despite any short-term windfall for investors. This did not prevent certain mill owners from becoming adept at manipulating the legal system for competitive advantage. When an upstream mill diverted the river’s flow under the guise of maintenance and decreased water pressure to the point that its downstream competitor could no longer drive its millstone, the downstream company sued in court and won. But the upstream defendant appealed to King and Parliament in faraway Paris and succeeded in dragging out the case for close to fifty years so the plaintiff was forced out of business and its assets acquired by the defendant at pennies on the dollar.

Operations

Because shareholders invested for long-term growth with shares passed down through generations, and because managers were not rewarded based on quarterly earnings per share, there was little motivation to forgo maintenance or skimp on capital expenditures in the name of short-term gain. As a result, the mill companies kept growing and commerce in the region took off with Toulouse becoming one of the early industrial centers of Europe, particularly in textiles whose manufacture came to depend on power generated by the mills.

Keeping the machinery running was a constant challenge in an era when engineering in the modern sense was just beginning to take hold. A top priority was generating cash flow to fund repairs and capital improvements. Because farmers paid in kind (one-seventh of their grain) to have their wheat ground into flour, the mills’ customers were not a source of cash. To raise cash, the shareholders could authorize a reinvestment of these profits-in-kind that, when ground into flour, were sold to local bakers. But investors wanted a better alternative. In an early example of business diversification, the mills generated cash by charging local fishermen for the right to fish at the dams built by the mills, where fish were plentiful and easier to catch. This revenue became so lucrative that the mills came to the attention of the King, who was given a one-half interest in the profits, a “royalty,” in the hope of averting a government takeover.

A significant challenge became how to preserve the grain until it could be doled out as a dividend to shareholders. Although it was measured and distributed several times a month as a dividend-in-kind, the volume of what went out was always less than what came in, owing to the natural drying process along with rats and insects that ate into profits. While this problem was not resolved in the Middle Ages, it led to increased emphasis on accountability and accelerated distribution of dividends, which continued to be paid in-kind until 1840.

Financial

Shareholders’ concerns about not getting their fair share of profits gave birth to innovations still at the heart of modern business and corporate governance – transparency, internal controls, and the independent auditor.

The board had to balance the shareholders’ short-term self-interest in maximizing dividends and boosting the share price against the long-term prospects of the company, dependent on plowing profits into maintenance and capital improvements so the mills could run more efficiently and avoid costly breakdowns. This sparked the need for a reliable way to measure income and expenses. Adopting a method developed in Genoa, all transactions were recorded meticulously using a precursor of the double entry system of bookkeeping and combining, for the first time, the ledgers recording income and expenses to arrive at profit.

While overseeing the receipt of revenue was important, it was in the area of expenses that the greatest number of controls was instituted. For example, to remit a payment, the instructions had to be detailed and in a writing, including the address of the payee and the reason for the payment. All disbursements had to be approved by at least four authorized co-signers. Then the person receiving the payment had to sign for it, or if illiterate, had to find a notary to sign on his behalf. To further police outlays, the person recording an expense in the general ledger could not be someone who had authorized it.

It was concern over reliability in tracking revenue and expenditures that gave rise to the role of the independent auditor. Unlike today, auditors were hired by and reported exclusively to the shareholders – not to the board or to management. They reviewed the accounts, insisted on back-up for each transaction, and stood behind the financial statements. As a result, the shareholders knew what profits to expect and this had a direct impact on the market value of their shares and the companies’ ability to attract new, long-term investors.

Without access to global financial markets, the shareholders remained responsible for raising funds by reinvesting profits, contributing supplemental capital, and authorizing the sale of additional shares. Shares were issued only to individuals. They had to be sufficiently well off to take the risk of contributing additional funds when more capital was needed, since shareholders and other related parties were prohibited from lending money to the companies. While occasional short-term borrowing from unrelated lenders was permitted for emergency repairs, there was no such thing as a line of credit or an overdraft facility. The mill companies did not invest in other enterprises nor did they mortgage their real estate to obtain funds. Financing expansion and improvements depended solely on profitability.

The companies’ finances were helped by the County of Toulouse in a form we would recognize today as a property tax abatement. In exchange for the mills’ role in infrastructure and defense, as well as the importance of flour for making bread and feeding the local populace, the companies were granted exemptions from the tax on real property and so had more cash to invest in maintenance for improving reliability and being good corporate citizens.

Human Resources

It was a challenge for the board to find and retain professional managers having the technical knowledge to keep the mills running while supervising the employees and serving customers. Mill managers were kept on a short leash to maximize profits but also to avoid abusing workers who were tough to replace. Granted one-year contracts, managers’ performance was reviewed at the annual general meeting of shareholders. Managers were personally liable for any shortfalls in the accounts, while their reward for a job well done was another one-year contract.

Conflicts of interest, deemed among the most significant threats to the enterprise, were averted through a set of simple yet effective mandates. Rules were instituted prohibiting employees and their families from dealing in grain or from buying shares in the company. Neither shareholders nor their family members could be employees. The board was limited to shareholders, with no seats for management or outside directors. Demands by employees for profit-sharing were quashed. Shareholders and employees were forbidden to lend money to the corporation, and vice versa.

In an era before labor unions, management had the upper hand even though workers could be scarce during a period of global cooling when harvests failed and the Black Death recurred, resulting in an average life expectancy of just 30 years. Working hours were from dawn to dusk. Strikes were prohibited. Employees had to swear an oath at the beginning of each year to abide by company regulations, and if they failed, to pay a fine.

Information Technology

From the records, it appears that information technology was focused primarily on financial data such as the shareholder registers, ledger books, and meticulous records of receipts and expenses preserved to this day. Creating and maintaining an audit trail, along with the ability to monitor compliance with procedures and policies, were key to supporting the transparency shareholders demanded.

At a time when land transportation was perilous and slow, the rivers and waterways of France were the information superhighways of their time. Particularly during the Gothic building boom, knowledge sharing and innovation were based on itinerant architects and masons moving from town to town and bringing with them their models and tools. This technology had its impact on the mills as well, whose infrastructure had to withstand attack. Attached to dams supporting bridges across the rivers that powered them, the mills were strategic military assets that had to be sturdy and defensible within the context of the 14th century arms race. This meant constant inspection and paying for upgrades based on improved technology whenever it happened to become available.

Sales and Marketing

One area where there is little information in contemporary records is sales and marketing. Given the efforts that went into keeping competitors from operating in close proximity and disrupting or distorting the flow of the river to a mill, marketing took a back seat to maintaining market dominance and to being the only mill in town. Depriving consumers of choices prevented the need for much effort or expense to increase sales.

Assuring customer satisfaction was, however, a significant aspect of the business. At a time when flour was easily contaminated by insects and by rat droppings, or could be adulterated with fillers, mill managers were charged with ensuring purity and the reliable measurement of the farmers’ sixth-sevenths share of the grain being ground. Shareholders recognized the importance to the bottom line of customers’ perceptions and confidence, driving their board and managers toward zero tolerance for error.

Lessons from Medieval Times

Throughout the 14th century, two central themes emerged – the supremacy of shareholders acting through their board of directors, and their commitment to transparency in corporate governance supported by strong internal controls and third-party audits.

It may be easy to dismiss as simplistic the accomplishments of these medieval pioneers when today’s companies have millions of shareholders instead of 80 and operate around the globe rather than in one river valley. But if the corporate governance established in the late Middle Ages had been in place during the last few years, it is tempting to speculate that fiascoes sparking the Sarbanes-Oxley legislation and the more recent turmoil in global financial markets might not have occurred. In a time before EBITDA, collateralized debt obligations and credit-default swaps, with nary an investment banker in sight, medieval Frenchmen using common sense and an innate understanding of human nature embraced self-regulation and transparency to earn the confidence of the investing public. The mechanisms they created stayed in use, virtually unchanged, until the French Revolution while the mill companies built the generators powering the industrial revolution and eventually the hydro-electric plants of 20th century France. They would be with us today had they not encountered an immovable force in the aftermath of World War II -- the French government’s nationalization of the electrical grid and the monopoly known as Electricité de France.

*This paper was prepared to accompany a presentation delivered at the McGeorge International Law Conference in Rome, Italy on May 26, 2012. It is based on Aux Origines des Sociétés Anonymes – Les Moulins de Toulouse au Moyen Age by Germain Sicard (Centre de Recherches Historiques, 1953). At the time of this conference, Meril Markley was International Tax Principal at UHY Advisors TX, LLC in Houston, Texas and Chair of the Tax Special Interest Group for UHY International. A.B. Vassar College (Phi Beta Kappa); J.D. University of Cincinnati College of Law; LL.M. Transnational Business and Tax, McGeorge School of Law (Sacramento, CA and Salzburg, Austria).